Shortly after Monday's meeting between Russia and Saudi Arabia on stabilization of the oil market, the oil prices jumped 5%. But not for long. As it became clear that this is yet another "hoax" promise from the oil giants, the prices drowned again.

This Monday, Brent (NYMEX: XBR/USD) reached the level of $49.40 per barrel on the news of the agreement, only to fall back to $47 shortly after. As investors realized that the publicized meeting of the two oil giants is nothing but the "cheap talk", the prices went back to their previous level. A lot of countries were calling for an international agreement to cap the oil production as a way to stabilize the oil prices, after the oil was hitting the bottom of $26s this year, causing economic distress. However, as the Monday's meeting between Russia's and Saudi Arabia's oil ministers went no further than signing an oil-cooperation pact, it seems that the long-awaited agreement to freeze the crude oil production is nowhere to be seen.

Even though the nations gathered a big publicity around the "historical" meeting, both countries refrained from making any decisions and said that there is no urgent need in limiting the oil output at the moment. That's why a lot of analysts saw this "historical" meeting as nothing but a "lip service". Bloomberg cites the analyst Eugen Weinberg who believes that the market should not expect any real cooperation between the big rivals, as freezing the oil production would mean losing the leading position for both nations.

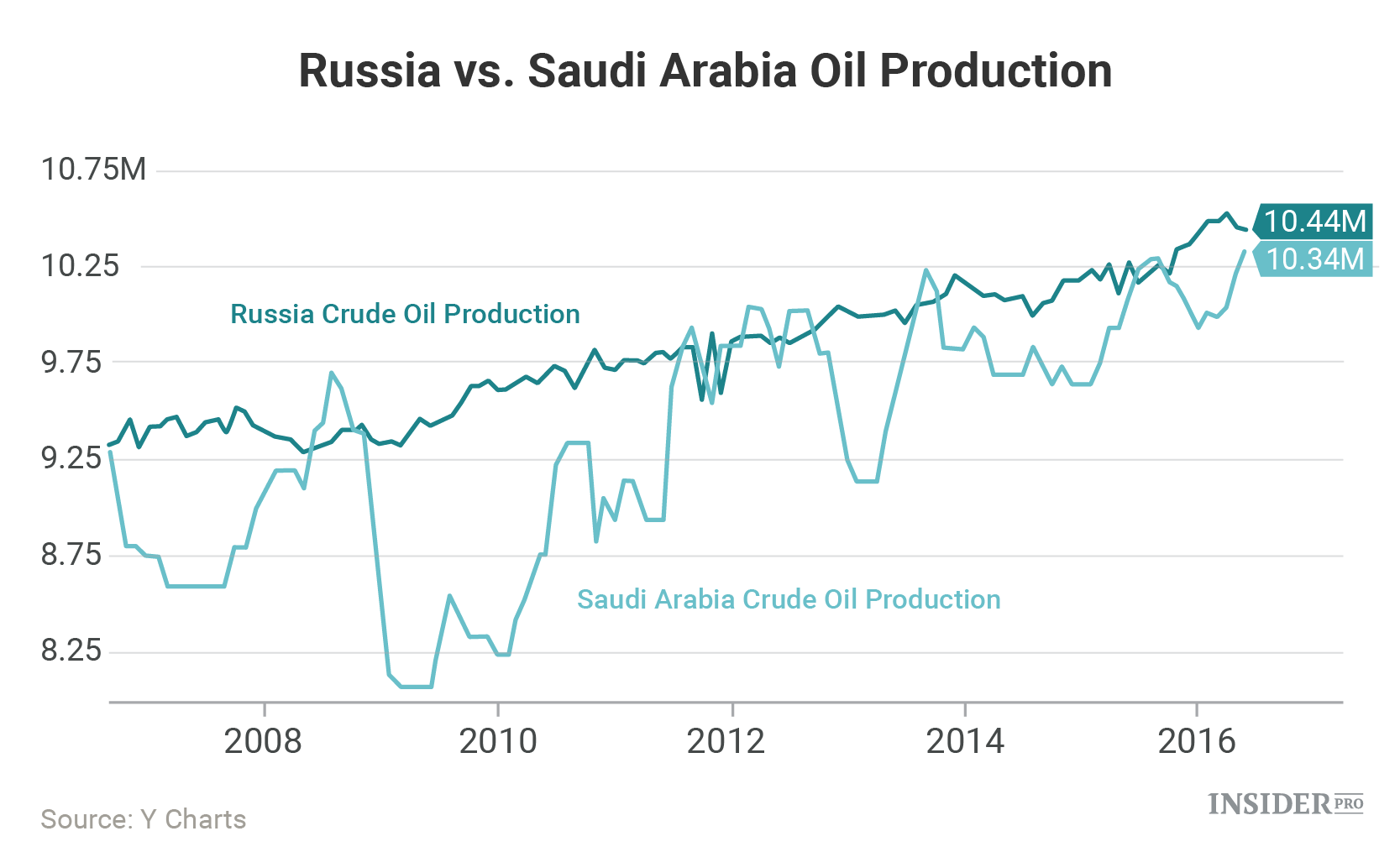

Another thing to consider before discussing any projections for 2017 is that both countries are pumping oil at the record high levels at the moment. According to the Russian Energy Ministry's report from yesterday, Russia's oil production exceeded 11 million barrels per day for the first time since 1991 in the past days. Likewise, Saudi Arabia, the biggest oil producer among OPEC countries, produced a record 10.69 million barrels per day last month. It doesn't look like any of these countries are interested in freezing the production right now.

"A freeze doesn’t resolve anything if Saudi Arabia and Russia are both freezing when their production is at a record high," analyst Saad Rahim told Bloomberg.

This chart reflects the oil production levels of Russia and Saudi Arabia as of the end of last week.

{kind=link}

Add to this the post-sanctions position of Iran, trying to make up for the economic losses after suffering from economic limitations. That is why, the experts expect Iran to only stir up the oil production to higher levels in the next months. Reuters reported that Saudi Foreign Minister Adel al-Jubeir has claimed to agree to participate in the oil production freeze if other oil countries would show initiative and come to an agreement on the issue. However, he believes that Iran would be the one to spoil it.

"I believe again the spoiler will be the Iranians. You can't expect other countries to freeze while you reserve the right to increase your production," Adel al-Jubeir told Reuters reporters.

Bloomberg says that it has always been Iran and Iraq's goal to substantially increase the oil production in their countries. And this would provoke Russia and Saudi Arabia to stir up their production rates, too. See where it's going to?

Hardly anything good to expect from 2017

In the light of these announcements from the oil-producing countries, it seems that the oil production is currently overwhelming the actual demand, and it's only getting worse. The market has been talking about stabilization of the oil prices for years, yet it still didn't happen. Is there hope that it will finally happen next year? The experts are not so positive about that.

Wim Thomas, the Chief Energy Advisor of Shell, believes that the large oversupply of oil that the market is experiencing right now, may not come to balance with the demand until the end of 2017. He told Reuters that the oil prices will be having a hard time getting back to the satisfactory levels if the countries continue fighting for the market share rather than for the balance.

Since 2014, the oil prices fell more than 70% and the ongoing overproduction of oil, aggravated by the smaller countries such as Libya, Nigeria, Iran and Iraq, is not expected to stabilize anytime soon. Well, unless the agreement on freezing the production actually happens.

Saudi Energy Minister Khalid Al-Falih mentioned that the country has the means to pump even more oil, at approximate levels of 12.5 million barrels per day.

“The market is now saturated with stored crude at beyond usual levels and we don’t see in the near future a need for the kingdom to reach its maximum capacity,” Al-Falih said.

Nevertheless, this capacity exists. Likewise, Russia said they can increase the production to the same levels as Saudi Arabia, if needed. All this looks like a threatening situation for the oil prices that are already 50% below the 2014 levels.

In the past months, the countries were battling to be the highest oil-producing country. But is this what the market needs? If the countries keep on producing at these levels, next year will not demonstrate any stability in the oil prices, far from it. And, as Russia has already learned the hard way, unstable oil prices lead to unstable economic situation for a heavily oil-dependent country.

Therefore, according to some experts, it will not be until late 2017 that the oil-producing countries finally come to any meaningful agreement on freezing the production in the interests of the market stability. That's why, investors should not expect any rebalancing in the oil prices anytime soon and be prepared for continued roller coaster.