A major criticism of those who doubt the worth of crypto is its lack of yield. Bitcoin, like gold, goes the argument, has no interest-bearing property.

But as the yield-farming craze gathers pace as an outgrowth of staking, typically of tokens that are staked to access network resources, services and governance, depending on protocol.

And if you have been following trends in the crypto space you will know that hundreds of millions of dollars in value is staked in the burgeoning breed of DeFi smart contracts that automate lending and borrowing, liquidity provision and the setting of interest rates, all by leveraging the wonders of algorithmic interest protocols.

However, taking part in yield farming means exposure to high risk, as speculators attempt to maximize returns by setting in motion a chain of contractual arrangements on decentralized exchanges where yield from one circuit becomes the input in a new circuit and its yield (all compounded as we go) an input as reward either for a liquidity provider in an automated market maker network or a borrower on a protocol that rewards for taking out a loan.

Yield-farming may be a bubble that will inevitably burst, but for now this part of the DeFi sector is in fine fettle. Yet, there are many who would prefer less high-octane approaches to earning interest.

Take a look at crypto savings accounts

It just so happens that there are ways to earn interest on your crypto that have been around longer than the yield farmers, and involve far less risk - and that’s by opening a crypto savings account.

A crypto interest account operates much the same way as the savings account you have with a regular bank. However, instead of depositing cash to earn interest on your dollars or euros, you deposit crypto assets and earn interest in return – although some platforms do offer interest on fiat currencies.

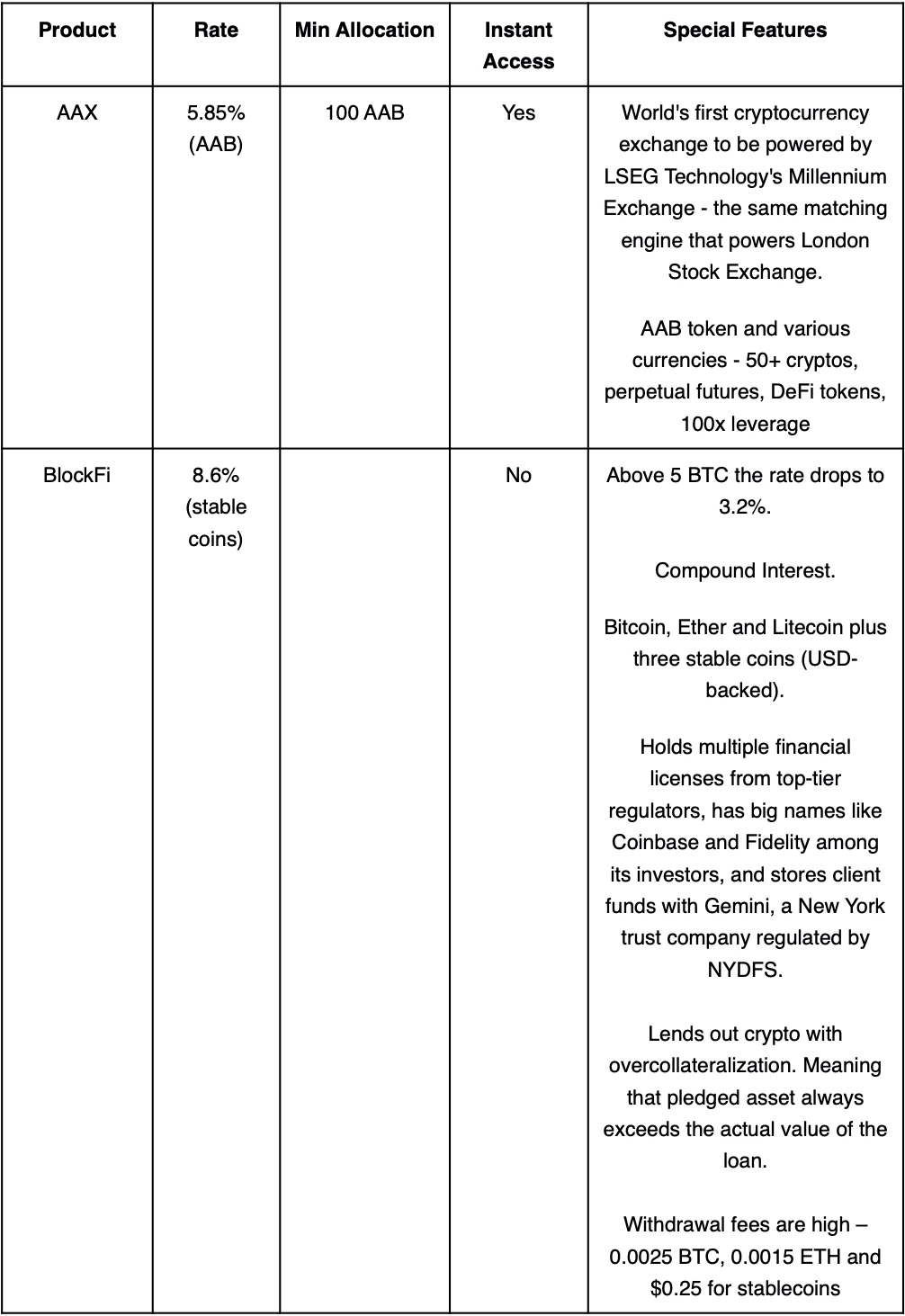

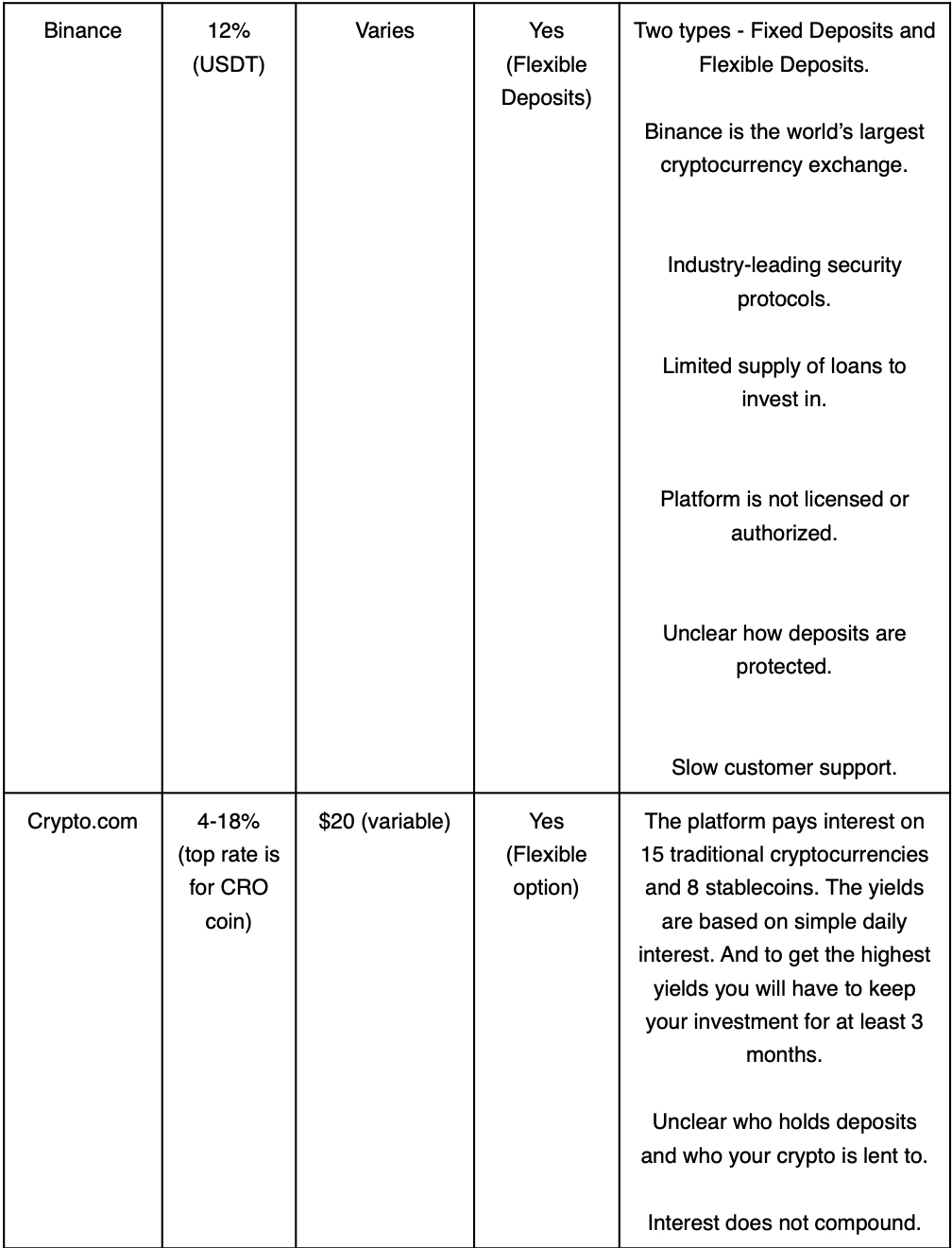

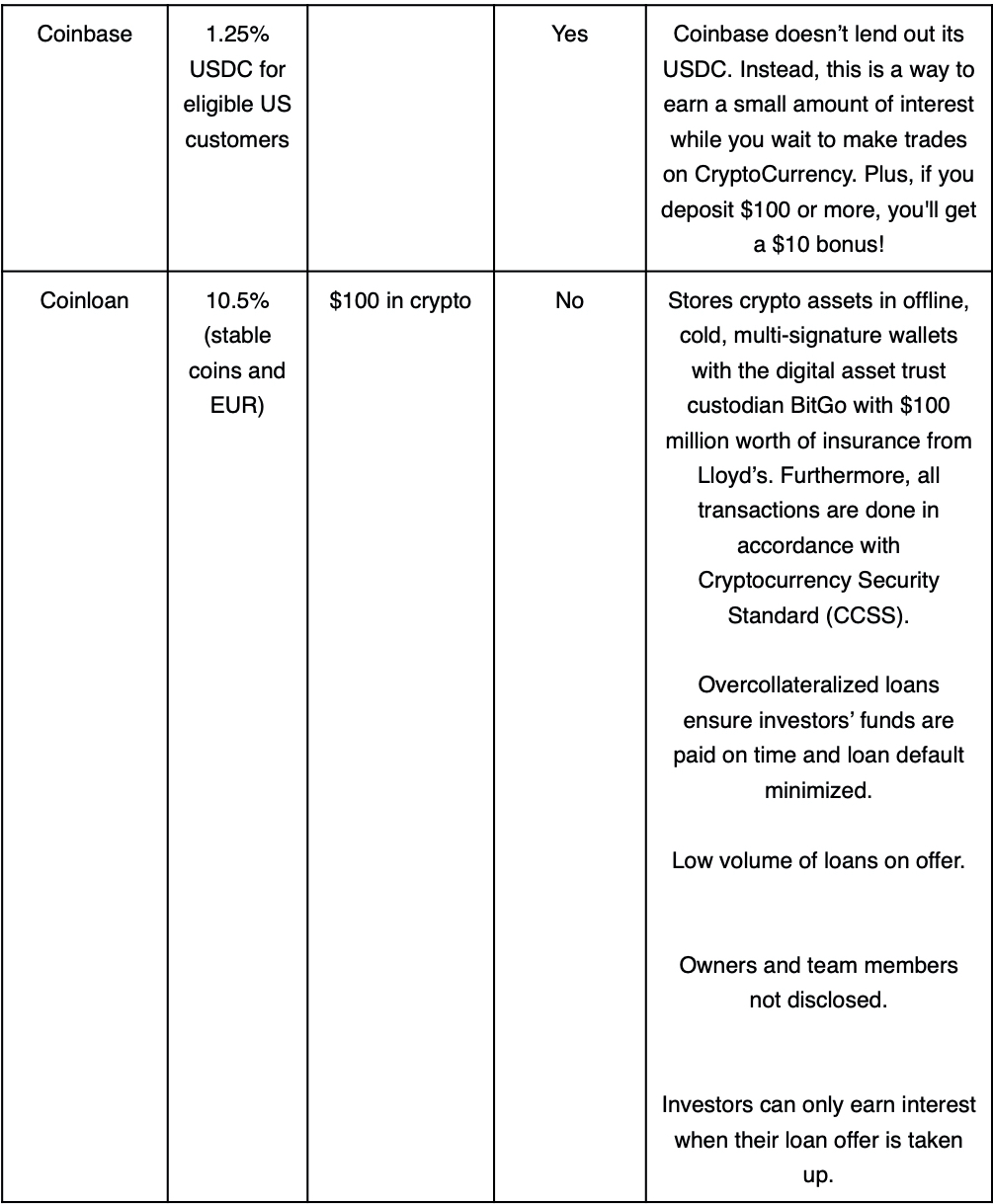

The big players in crypto savings include some familiar names, such as Coinbase, BlockFi, Binance and Crypto.com. As of this month there will be a newcomer in the shape of AAX, the two-year-old institutional-grade Maltese exchange, part of the ATOM Group, now launching a crypto savings account with instant withdrawal that earns depositors a 5.85% interest rate.

AAX launched its AAB trading discount token in April this year and volumes in August.

No blackout

A unique aspect of AAX’s offering is its deployment of the same matching engine that powers the London Stock Exchange - LSEG Technology's Millennium Exchange (a matching system is the core of all financial instrument exchanges.)

With its resilient tech stack and top-line security, AAX boasts constant uptime as a competitive advantage, so it says there’s no blackout for clients to worry about it.

Savers with AAX will no doubt be comforted by the market efficiencies the platform’s technology brings. The exchange spans OTC, spot and futures.

If a company (exchange in this case) fails, for example after suffering a fatal security breach, you can lose your money. In such a risk context institutional-grade systems are a key benefit. You should think of a crypto savings account as more of an investment rather than a savings account - there’s no FDIC insurance to come to the rescue.

Interest for keys and the centrality of custody

There are some fundamental differences between crypto and fiat savings and the question of custody throws that into sharp relief.

In a normal savings account, the money is yours. In a crypto-based savings account, your crypto keys are lent to others who can use the crypto for a certain period of time. In exchange, the borrower promises to pay you interest on the crypto that you lend them.

There are of course those crypto enthusiasts who for good reasons stand by the mantra "not your keys, not your crypto," which emphasizes that entrusting your keys to an exchange or other third party means a loss of self-sovereignty.

Although self-sovereignty has its own downside, given that most people still hold crypto on mobile devices – losing your phone could mean losing all your money. Even if you have multi-factor authentication on your wallet, you could lose everything.

However, as crypto has matured custody services have come on stream to meet demand for custody solutions from crypto holders. And exchanges such as AAX are looking to assuage the fears of the key sovereignty crowd by paying interest but also by providing rock solid security.

Crypto bank services like AAX’s have built-in redundancies to secure the crypto keys. These institutions take bank-level security to the next level. AAX for its part in addition to full and constant market surveillance, has also teamed up with Kroll for robust cybersecurity defenses.

This is important because with crypto savings accounts, when you deposit coins, you give up access to your keys. That allows the exchange to lend your crypto to other individuals.

As we’ve seen, some crypto investors find this to be unacceptable, so they choose to avoid savings accounts altogether. But in so doing, those shunning crypto savings are missing out on high yields for minimal risk.

Why crypto savings yields are higher than fiat

Yields on cryptocurrencies are higher than the yields on traditional savings accounts. This is because crypto banks cannot inflate the money supply, so they have to attract investors with high yields. The supply and demand for crypto financing drives the interest rates. And it gets better.

As an investor, your deposited digital assets are loaned to borrowers at an agreed interest rate. The borrowers secure their loans with crypto assets, which are usually far above the loan value. This is known as overcollateralization, and is the basis for crypto lending.

Overcollateralization ensures the loans are paid back on time and in full. Due to the volatility of cryptocurrencies, the collateral is monitored, and borrowers are advised to repay part of the loan or increase the collateral if the value drops to a predetermined level.

There’s at least one other good reason for taking a look at crypto savings: it beats keeping it in a wallet yielding nothing.

When you have Bitcoin or another form of crypto in a wallet, the number of coins you own doesn’t change over time. With crypto-based savings accounts, the number of coins you own will increase over time.